This article first appeared on the Bretton Woods Project.

The world is experiencing the “biggest investment boom in human history”, with some $6-9 trillion annually (8 per cent of global GDP) devoted to mega, giga and tera (million, billion, and trillion) dollar projects.

World leaders, specifically the Group of 20 (G20), are staking their reputation on achieving a growth target – namely raising global GDP by 2.1 per cent over current trajectories by 2018. The G20 sees massive infrastructure investment as one of the ‘silver bullets’ that can achieve its target and, by boosting trade and integration, add $2 trillion to the global economy and create millions of jobs.

The private sector, a major driver of the boom, suggests that about $60-70 trillion of additional infrastructure capacity will be needed by 2030 (see Business 20 recommendations). Under current conditions, public and private investments could provide about $30-35 trillion and $10-15 trillion, respectively, leaving a gap of $15-20 trillion. Policy-makers see long-term institutional investors, such as pension funds and sovereign wealth funds, as the key to bridging the gap. These investors control about $85 trillion and seek higher returns on their money, such as infrastructure can provide.

Another major driver of the boom is competition between the ‘West and the rest.’ As described below, the US-led World Bank is one of the institutions in the vanguard of this competition. When Jim Yong Kim assumed the World Bank presidency in 2012, staffers reported that he was presented with “Big Development” and “Small Development” approaches. Kim leans toward “Big Development” – or “transformational” projects.

In fiscal year 2014, World Bank Group financial commitments rose by 17 per cent to $61 billion. This is consistent with the institution’s pledge to double its volume of operations within the decade. Infrastructure-related commitments represented about half of all World Bank (the Bank’s middle income and low income arms, the International Bank of Reconstruction and Development and the International Development Association) commitments and 40 per cent of all World Bank Group commitments, including the Bank’s private sector arm, the International Finance Corporation (IFC) and the Multilateral Investment Guarantee Agency (MIGA).

The Bank aims to ‘square the circle’ by investing more money in bigger projects with a smaller staff while, at the same time, meeting its goals of ending extreme poverty by 2030 and boosting shared prosperity for the poorest 40 per cent in developing countries. Meanwhile, oversight of operational impacts on the poor and the environment are declining since 2012, when the Bank decided to apply the IFC’s performance standards, rather than the Bank’s safeguards, to its investments in PPPs. Performance standards put the burden on developing countries to ‘do no harm’, with limited oversight by the World Bank itself.

A 2014 review by the Bank’s Independent Evaluation Group looking at 128 World Bank-financed public-private partnerships (PPPs) found that: “PPPs generally do not provide additional resources for the public sector.” The review noted that the main measure of ‘success’ is profitability – other factors are rarely considered. With this measure, 62 per cent of its PPP transactions were rated satisfactory or better, although the failure rate in certain sectors were high: water (41 per cent) and energy distribution (67 per cent). Alarmingly, “contingent liabilities [i.e. risks to national treasuries] are rarely fully quantified at the project level.” Citizens should protest the Bank’s obliviousness to the impact of such budget liabilities (which offset corporate risks) on their systems of taxation, pensions, and user fees over the course of generations.

Joining forces: Seven MDBs and the IMF

In addition to its own expansion, the World Bank Group is exploiting synergies with other institutions in an unprecedented way. Two days before the G20 Summit in mid November, seven multilateral development banks (MDBs) and the IMF wrote a collective press release announcing:

- Their combined capacity to provide $130 billion in infrastructure financing annually;

- Their intention to strengthen existing Project Preparation Facilities (PPFs) and create new ones which will speed up and replicate the launch of mega-projects. The capacity of PPFs to ‘super-size’ projects will address the “critical barrier” to boosting infrastructure investment – namely, “an insufficient pipeline of bankable projects ready to be implemented”; and

- The creation of the Global Infrastructure Facility (GIF) at the World Bank’s October 2014 annual meetings.

The Bank-hosted GIF is a partnership including other MDBs and 16 private sector partners and financial institutions (e.g., Blackrock, Citibank, HSBC, World Pension Council) representing over $8 trillion in assets. The GIF’s mandate is to: (a) leverage private sector investment; (b) address public goods; (c) partner for solutions; and (d) financialise infrastructure as an “asset class”. The GIF could be the ‘mouse that roars’ insofar as the intention is to use its tiny initial capitalisation of $80 million (and future capitalisations) to introduce a new model of financialisation wherein the public sector ‘de-risks’ projects to attract long-term institutional investors (e.g. pension funds).

The role of the IMF is to prepare a paper for its board that will set out “guidelines on strengthening public investment management practices across countries at differing levels of development.” The IMF got internal pushback for its cautionary approach to infrastructure in its October 2014 World Economic Outlook. For decades, policy leaders have tried to force collaboration among the MDBs and the IMF without much success. The breakthrough may be inspired by recent actions taken by China and other emerging market countries. Working collectively, the MDBs can probably outspend any other development finance institution (DFI), except for the China Development Bank.

Keeping pace with China is a US priority. According to the US-based think tank the Center for Strategic and International Studies, in 2014, “Beijing mounted the first serious challenge to the US-led global economic order established at Bretton Woods 70 years ago.” For instance, in the last half of 2014, China led the formation of the Asian Infrastructure Investment Bank (AIIB) and about six other infrastructure initiatives. Shanghai will host the New Development Bank of Brazil, Russia, India, China and South Africa (BRICS), although the bank’s governance is engineered to help balance power among the founding members.

Perhaps the sheer scale of infrastructure initiatives led by emerging market and Western countries prompted the G20 to downsize its own ‘global infrastructure initiative’. Initially, the G20 Global Infrastructure Hub was to move trillions of dollars over 15 years for an agenda that sounds similar to that of the GIF. This may still be possible. But, today, the Hub is a four-year pilot programme run by a non-profit organisation located in Sydney, Australia, with an annual budget of $15 million. Seed capital was contributed by eight countries (Australia, UK, China, Saudi Arabia, New Zealand, South Korea, Mexico and Singapore).

The policy nexus: Infrastructure, integration, trade, extraction

On each continent, the G20 and the DFIs pursue infrastructure strategies in tandem with integration and trade goals. Especially where countries lack creditworthiness, it is common to arrange an exchange of infrastructure for a revenue stream from an extractive industry. For instance, in Africa, the World Bank is launching a $1 billion map of geodata which “will unlock the true worth of Africa’s mineral endowment”.

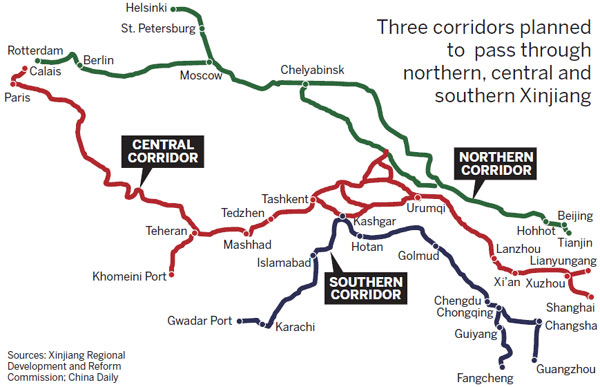

Selected maps of proposed investment by the World Bank and other institutions in Africa, South America, Central America and along the ‘Silk Road’ in Asia, demonstrate the nexus between infrastructure, integration and trade. They also demonstrate how the idea of ‘appropriate scale’ development, which is suited to the local/global ecosystems and the affected citizenry, seems to have gone ‘out the window.’

{kind=link}

At the country level, the World Bank’s staff assessment of the growth strategies of the G20’s emerging market economies demonstrates how the priorities relating to trade, integration, infrastructure and labour flexibility are inter-twined. On infrastructure, the Bank pushes countries to mobilise private capital, recover costs, standardise regulatory frameworks, and build the capacity and targets for launching PPPs. There is no mention of renewable energy or energy access.

Four key elements of the new infrastructure investment model

The sharp policy focus of donors and creditors is on using public money to ‘de-risk’ projects in the early stages of preparation in order to attract private investors, especially long-term institutional investors (such as pension funds), which will earn long-term stable returns (estimated at 20-25 per cent) over the course of generations. As Bent Flyvbjerg of Oxford University states, the “iron law of megaprojects” is laid out and documented: “Over budget, over time, over and over again.” Because of this, the model poses a danger of socialising risks and privatising gains and, thereby, accelerating already obscene levels of inequality (see element 4, below, for a description of how inequality is created).

The four key elements of this model involve:

1) Creating an ‘enabling environment’ that harmonises laws and regulations among countries in ways that attract and protect private investors, especially in infrastructure PPPs. Harmonisation is key because many mega-projects involve multiple countries; they may also consist of more than 500 sub-projects. An enabling environment will discourage a shift in tariffs or in social or environmental regulations that impact an investor’s bottom line. The World Bank’s Doing Business report pressures nations to unify laws and regulations by, for instance, downgrading a country’s ranking when it does not protect contracts or increases taxes. Harmonisation has also involved erosion of domestic legislation and sovereignty.

2) Identifying infrastructure mega-projects (eg energy, transportation, water) that promote economic integration and trade on a regional, continental and global scale. For example, in 2011 the G20’s High-Level Panel on Infrastructure’s report recommended criteria for selected mega-projects that emphasise the readiness or maturing of projects and their potential for promoting regional integration and advancing liberalisation. The World Economic Forum has more elaborate processes for selecting projects. These processes seek to inform civil society on the results rather than involve them in the processes.

3) Aggressively using new and existing PPFs to prepare and fill “pipelines of bankable projects” in each geographical region. PPFs are competing to ‘super-size’ projects by, for instance, compressing the time for project preparation from seven to three years; expediting land acquisition; and standardising bidding, procurement and other processes. A September 2014 G20 report is alarming because it describes how PPFs in Africa and Asia will expedite the replication of projects in ways that sideline citizens – the purported beneficiaries.

(4) Mobilising public money (e.g. taxes, pensions, aid) to offset the risk of private firms, including long-term institutional investors. Given the fiscal incentives offered to investors, including “contingent liabilities” (or budgetary set-asides) to offset corporate risks, nations could be faced with unprecedented levels of risk as these investors pool financing of portfolios of PPPs. The pattern of socialising risk while privatising profit accelerates levels of inequality.

Importantly, the DFIs are acting more like investment banks than development banks and, thus, duplicating the role of the private sector. For instance, civil society has qustionned whether the IFC’s funding has leveraged resources that would not have otherwise been available.

The first three elements of the model are not new, but the scale and mechanisms for promoting them are. The fourth element – potential mobilisation of trillions of dollars from institutional investors – is a ‘game changer’ that would transform the accountability relationships between the state and its citizens, on the one hand, and the large ‘pools’ of financial investors, on the other. This process is called “financialisation” of infrastructure as an “asset class”.

Bank president Kim and UN secretary general Ban Ki-moon share the vision of financialisation. In October 2014 Kim stated: “The infrastructure gap is simply enormous – an estimated $1 trillion to $1.5 trillion more is needed each year. To fill this gap, we need to tap into the trillions of dollars held by institutional investors – most of which is sitting on the sidelines – and direct those assets into projects that will have great benefit for a range of developing countries.”

Ban Ki-moon’s December 2014 synthesis report on the post-2015 agenda states that “Urgent action is needed to mobilise, redirect, and unlock the transformative power of trillions of dollars of private resources to deliver on sustainable development objectives.” Another influential August 2014 report to the UN General Assembly states: “Engagement in isolated PPPs, managed in silos should be avoided. The investing public entity should carry out a number of [PPP] projects simultaneously and thereby take a portfolio approach for pooling funds for multiple projects”.

If we remember that PPPs do not generally provide “additionality” (especially when corporate providers lack efficiency in delivery of services), the scale of the proposed public investment could undermine any attempt to achieve sustainable development goals. After the reckless lending of the petrodollar boom in the 1970s, governments were saddled with unpayable debts for generations. Such mistakes cannot be repeated.

Conclusion

Civil society must urgently ‘spread the word’ about the nature and magnitude of the infrastructure boom and build a platform to engage policy-makers and firms. By building a common platform, civil society can help ensure that discourse on the future of infrastructure, which shapes the path of development and locks-in technology for generations, is not divorced from the discourse about other concerns. These include a binding regime for curbing global greenhouse gases; sovereign and sub-sovereign austerity and indebtedness; taxation and corruption, safeguards and norms; global value chains; energy access; the path to sustainable development goals; and gender equality.

The ‘means’ to a sustainable world should not defeat the ‘ends’ – the goals of reducing poverty and inequality, achieving women’s rights, or ensuring a livable planet. In other words, the new development model must be transformed to deliver the public goods required for a sustainable future.